The history repeats itself crowd thinks that that there must be a bubble sooner or later. “Now?” they constantly ask, “Is it a bubble now?” as if history has to repeat whatever was most memorable about the last time. History may repeat itself, but there’s an awful lot of history that this particular venture capital cycle could repeat. Below is a short history of venture capital in the 1980s, my interpretation and comparison to the ’90s and today, and some thoughts about what that means. It’s long. If you’re attention-deprived, skip to ‘1980s v. 1990s’, about four-fifths of the way down.

To 1980

Baby, baby drove up in a Cadillac

I said, “Jesus Christ, where’d you get that Cadillac?”

– The Clash, 1979.

The Carter years were tough.

They started out well. The recovery from the 1973-1975 recession brought unemployment down and incomes up. But all this was undone by the return of inflation. By 1980, when inflation reached its peak, unemployment was rising, interest rates were at their highest levels since World War II, productivity growth had slowed, and business investment was falling. Fear ruled the markets, a “crisis of confidence” ruled the people.

Venture capital had a different trajectory in the 1970s: until 1978 there was almost nothing, then suddenly, it took off.

One of the reasons for venture capital’s current heady successes is the good judgment men like Burr [Craig Burr of Burr, Egan, Deleage] and Cronin [Dan Cronin of Ampersand Associates] learned while slugging their way through the near-dormant mid-’70s. The period between 1972 and 1978 may someday be remembered as venture capital’s years in the desert. After a heady adolescence in the late ’60s, the business almost disappeared from public view after the bull market of 1968-69 went into eclipse, taking with it the new-issues market that had buoyed the venture business. (Inc. Magazine, “The Billion Dollar Gamble“, 9/1/1981)

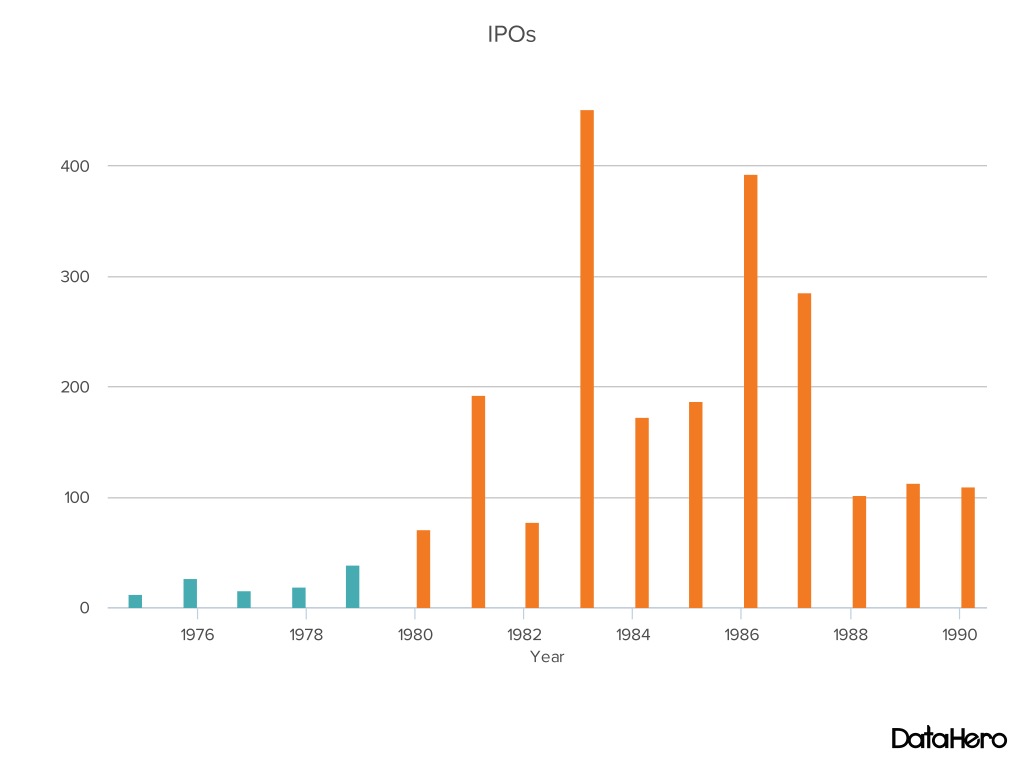

The pioneers of the 1960s and 1970s had figured out a winning formula: build a great network to source opportunities, spend months getting to know the management team and doing due diligence, invest at the earliest possible stage, work hard to help founders get the right team in place and put together partnerships, and take the company public only when it was ready to be a public company. The result was that, despite an IPO market that had virtually disappeared, iconic VC-backed companies made it out into the market. Cray and Tandem in 1976, Evans & Sutherland and Federal Express in 1978, and Apple and Genentech in 1980. The Reagan years looked promising.

The Accelerating Universe, 1980-1983

Never for money, always for love…

I guess this must be the place.

– Talking Heads, 1983.

By 1981 economic triumphalists were crowing that the ’80s were to be the “decade of the entrepreneur.”

It adds up to quite a boom, recalling the late 1960s. Though final figures aren’t tallied, about twice as many high-tech companies were started in 1980 as in 1979, drawn by the twin lures of plentiful venture capital and the dazzling market debuts of two former venture companies in electronics and genetic engineering: Apple Computer Inc. and Genentech, respectively. (Wall Street Journal, “Venture Capitalists Rush in to Back Emerging High-Technology Firms”, 3/18/1981.)

There’s so much money chasing these deals that venture capitalists are in competition with each other. They spend their energies marketing themselves instead of screening the deals. It’s gotten silly.1

Money had been pouring into venture capital since a 1978 change in regulations allowed pension funds to consider it a “prudent” investment. The $2.5 billion managed by venture capital firms in 1977 quintupled by 1983 to $12 billion.2 New money committed per year rose 16x over five years, from $218 million in 1978 to $3.6 billion in 1983.3 The number of venture funds grew from 47 in 1980, to 71 in 1982, to 113 in 1983. The number of investment professionals nearly tripled, from 597 in 1977 to 1,494 in 1983.

The economy started to improve. The new Federal Reserve Chairman Paul Volcker, appointed by Carter in 1979, had taken the politically unpopular move of raising interest rates to combat inflation, to 20% by mid-1981. It was painful, but it worked: by 1983 the decade of stagflation was over. The IPO markets celebrated with their biggest year since 1969. A Carter appointee had delivered on Reagan’s promise: it was Morning Again in America.

Venture investments got competitive, and more expensive. “We have less time to make up our minds,” said Eugene Kleiner in a Wall Street Journal article, “It used to be that you had two or three months. Now it’s a matter of weeks or even days, because if we don’t somebody else will.”4 VCs started to invest ever earlier in a company’s lifecycle to try and avoid competitive term-sheets.

More and more these days, venture capitalists are financing the birth of new companies. The typical venture-capital concerns used to provide money only after a few hundred thousand dollars or more had been put into a business by relatives and principals, and only after the company had a product well along in development. But now the values of young companies are rising so rapidly that venture capitalists who invest at the traditional stage often can’t make the five to tenfold profit they typically require. (Wall Street Journal, “To Increase Profits, Venture-Capital Firms are Investing Earlier in Fledgling Concerns”, 10/31/1983.)

The later stages of financing are becoming very crowded, so the best opportunity is to come in with seed money, or to invest even before the company has a business plan.5

Prices for startups rose. “The price tags on such companies are running from 20% to 100% higher than last year’s first-round financings,” said the Wall Street Journal in 1981.6 Some attributed the rise in prices to lack of experience.

A tendency by newcomers to overestimate the value of new companies has contributed to the recent sharp rise in the size of some deals…some veterans are dropping potential deals because they’re wary of the competence of other venture capitalists involved in the deal. (Wall Street Journal, “Venture Firms Lack People of Experience”, 12/8/1983.)

Almost two-thirds of VCs in 1983 had not been in the business five years before, they had very little venture investing experience. And yet the amount of capital each managed doubled, on average, from $4 million in 1977 to $8 million in 1983.

Half the people in the industry have only two years’ experience. “That isn’t sufficient at all.”

— Chris A. Eyre, Merrill, Pickard, Anderson & Eyre, Dec. 19837

So the 1983 IPO window was a godsend. Amgen, Biogen, LSI, Apollo, Compaq, Lotus Development, Businessland, Trilogy, Stratus, Paychex, Chiron, and a host of other VC-backed companies went public in 1983, far more than in any year previously. Industry folklore reported investment returns of between 30-50% per year.8 It was a watershed year for venture capital.

Naturally, that’s when things started to go wrong.

Heat Death, 1984-1992

There’s bum trash in my hall and my place is ripped

I’ve totaled another amp, I’m calling in sick

It’s an anthem in a vacuum on a hyperstation

Daydreaming days in a daydream nation

– Sonic Youth, 1988.

The bull market for tech stocks was short-lived. In 1984, the Wall Street Journal noted

“High” and “tech” are still a pair of four-letter words to a lot of money managers and individual investors. They remember the high-tech bubble of 1982 and 1983, when infinite price/earnings ratios were commonplace and anything ending in “onics” was oversubscribed. They also remember the high-tech crash of 1984, and the screams of pain up and down Wall Street. (Wall Street Journal, “High-tech Issues Again Begin to Brave Perils of the Once-Fertile Market for Initial Offerings”, 11/13/1984.)

This wasn’t a bubble. Prices had briefly gone up, as the Journal had noted in 1981, and then they declined:

For the first time since the boom in venture capital began five years ago, prices are falling in all stages of high-technology finance. Venture money is still abundant, and the private market value of some young companies are continuing to rise. Overall, however, venture investors are paying 20% less for deals than a year ago; for companies that haven’t lived up to their promise, prices are off by 50% or more. (Wall Street Journal, “Venture Capitalists Pay Less to Invest in High-Tech Firms”, 5/4/1984.)

In 1984 companies suddenly found it was again hard to go public.

1986 was a bit better, and firms like Microsoft, Oracle, Sun, Adobe, and Cypress Semiconductor took advantage of the opportunity, but the IPO market grew sluggish again after that. Tech IPOs peaked at 173 in 1983, a level they would not reach again for twelve years.

Venture returns started to fall. From a peak of about 30% median IRRs in 1982 and 1983, IRRs slid all the way down to about 8% in 1988.

The drop-off was entirely attributable to recently raised funds. Returns from funds raised in 1980 peaked in 1983 with an almost 20% cumulative return (the pre-1980 funds did even better.) 1981 was respectable. But funds raised in 1982 and after showed abysmal early returns through the ’80s.

Observers started casting blame: frequently on venture capitalists paying too much, or on inexperienced VCs.

Overpaying is an obvious explanation. Increased competition for deals may have driven prices up and returns down. But high prices in the early ’80s can’t account for the poor return of later vintages, so that can only be part of the explanation.

It’s also easy to believe that newcomers might just not be very good investors yet, that they would need some time to learn how to invest well. But poor returns weren’t limited to new VCs: returns broken out between first-time venture funds and follow-on funds show both the noobs and the experienced producing similarly dismal results.9

The poor performance of newer venture capital funds reflects that fewer companies are going public, and some are forced to go public at low prices.10

New money managers have a unique problem, though. They need to show they can make their LPs money before they go to raise a new fund. They need exits. Some observers claimed that new VCs were “grandstanding”: demonstrating their ability to exit by exiting too soon, especially through IPOs.11 By forcing their companies to go public before they were ready, they ended up with sub-optimal IPOs. This not only hurt the VCs involved, but it poisoned the well for other companies hoping to go public.

“Venture capital looked like a very easy business” in the boom times, but “venture capital has never been an easy business. There’s a lot of heartaches and a lot of hard problems to solve to create a durable enterprise.”

— Charles Lea, Dec. 198412

But the biggest problem, in hindsight, was that the sectors that had produced the best returns in the early ’80s were no longer delivering. Investors scrambled, betting on any idea that showed evidence of being able to become a winning business, no matter if it was technology or not.

The computer hardware boom had quietly ended as each category settled on an architecture. Soon after IBM released their personal computer in 1981, for example, the basis of PC hardware competition moved from product innovation to manufacturing and marketing efficiencies.13 Scores of companies trying to define what the personal computer would be were whittled down to just a few trying to market slightly faster and smaller machines to specific markets at ever lower prices. From PC design innovators like Apple, startup activity moved to efficient manufacturers and marketers like Dell and Gateway. Like the mainframe and minicomputer industries before them, and with the workstation market right on its heels, the PC hardware industry had moved from radical to incremental innovation.

So by January 1984 investors had turned away from hardware towards software.

Computer software companies are currently appealing to venture capitalists because their role in the personal computer industry is booming and appears somewhat less risky that the computer hardware market, which is undergoing a shakeout. (Wall Street Journal, “Software Companies Attracting Investors as Industry Booms”, 1/3/1984.)

But these VCs were already late to the market. By 1984 the big software wins of the 1980s were already founded or public. Computer Associates (founded 1974) went public in 1981; Lotus Development Corp. (founded 1982) in 1983; VM Software (founded 1981) in 1985; Adobe (founded 1982), Oracle (founded 1977), and Microsoft (founded 1975) in 1986; BMC (founded 1980) in 1988; Electronic Arts (founded 1982) in 1989.

The people who knew better noticed this immediately. Just a month after the previous article, the Journal reported Mitch Kapor saying “There are going to be some major nose dives, some will pull out, some will crash and burn.” Robin Grossman of Sevin Rosen Management, one of the top VC firms of the era, said “Venture money is already drying up…lots of investors will be disappointed.”14 Just nine months later, in November 1984, Benjamin Rosen, arguably the best VC of the era, wrote off the whole sector: “Soaring marketing costs, intense competition and an unfavorable stock market…make the success of new personal software companies highly questionable.”15

Over the past five years, venture capitalists have been chastened by large losses on an estimated $500 million in a dozen now-unsuccessful makers of mini-supercomputers.16

Other high-tech areas of focus also did not pan out. Despite being the natural evolution of decades of product trends, almost none of the mini-supercomputer firms survived. Artificial intelligence was a bust:

The AI industry, which many market researchers had projected would reach $4 billion in annual sales by now, remains nascent. Generous estimates of the market today are closer to $600 million. After swallowing up hundreds of millions of dollars in venture capital…hundreds of AI start-ups have yielded only a few profitable public companies. (Wall Street Journal, “Bright Outlook for Artificial Intelligence Yields to Slow Growth and Big Cutbacks”, 7/5/1990.)

Biotech, the great hope of the end of the ’70s, had fallen out of favor; progress was slow: the 1989 revenues of the top ten biotech companies was less than $1 billion in aggregate, with combined losses of about $33 million.17 Pen-based computing, interactive television, and superconductors did not pan out. Parallel computing was too early.18

The disk drive industry (called then “Winchester disk drives”) deserves a few paragraphs just by itself19 because it illustrates a recurring theme: VCs reacting to a few successful companies by massively over-funding the sector.

The success of one company in an area such as disk drives or semiconductors immediately spawned a plethora of me-too deals in the same business.20

The disk drive industry had been rapidly growing for several years. Few PCs had them in the early ’80s but they became standard as prices dropped. Between 1978 and 1983, sales in the OEM market grew from $27 million to approximately $1.3 billion, and were projected to continue growing to $4.5 billion by 1987. Companies like Memorex, Control Data, and Storage Technology were big winners. When it became clear how well they were doing, more companies were formed and funded.

Dave Marquardt…made a half-million investment in Seagate in May 1980. When Seagate went public in the Summer of ’81, that half-million was suddenly worth twenty million.21

In 1981, 12 disk drive companies were founded and received venture capital. In 1982, 19 companies; in 1983, 22 companies. Almost $400 million was invested in the industry between 1977 and 1984, $270 million of that in 1983 and 1984 alone. By 1983 there were more than 70 companies competing in the industry. In response to the increase in competition, prices were slashed and margins fell dramatically, but fixed R&D expenses did not. The valuations of these companies collapsed.

There are more than 64 floppy-disk makers. Perhaps that’s too many. That’s just a personal observation.

— Allan Krowe, IBM, June 198522

Venture investors have always flocked to sectors that begin to show promise. There were a plethora of funded PC manufacturers, for instance. Individual companies in these over-funded sectors still succeed,23 but overfunding causes overall low returns. In the 1980s this was exacerbated by the sheer number of new VCs, their fear of missing out on what might be a career-defining win, and the few promising sectors that appeared.

There are fewer high-tech deals that are perceived to be hot.

— Robert Kunze, Hambrecht & Quist, Feb. 198724

In retrospect, we can see new areas on the horizon: Cisco was founded in 1984;25 AOL in 1985; Thinking Machines unveiled its first massively parallel computer, the Connection Machine, in 1986. But it was not obvious at the time how these ideas would generate new markets; it was too early.

Speaking at the 1990 Venture Forum, John Doerr of Kleiner Perkins illustrated the industry’s frantic search for an innovative sector that could sustain it.

The business grew too fast, there were too many people trying to do technology start-ups.

— Kevin Landry, TA Associates, Nov. 198826

[Doerr] went on to contend that…pessimism is all wrong because the business is not a zero-sum game and several significant trends will create opportunities for billion-dollar companies in the 1990s. Doerr believes the most promising opportunities include instrumentation for human gene screening, the development of more effective pharmaceutical products for the aging population, a new generation of audiovisual, pen-based computing, new discoveries in neurobiology, and automated designer chemicals.27

If an interviewer asked John Doerr a few years later about the most promising opportunities, he would have had a clear and concise answer (Doerr backed Netscape and Amazon.com in the early ’90s.) But between 1984 and 1992 there was no clear answer.

Pension funds and others who stake VCs can’t really know how poorly their venture investments are doing until years after the fact. So even as returns on recent funds went negative in 1985-1989, money kept pouring into venture; VCs had to figure out something to do with it.

You might as well go for the safer and more current return because you do have the time value of money. I am being penalized for being a long-term investor.

–Steven Gilbert, Chemical Bank’s VC fund, May 198828

VCs figured that, absent blockbuster companies, IRRs could be improved either by shortening holding periods or having a higher company survival rate. Despite learning in the 1970s that early-stage investing is where the returns are, firms in the 1980s started to invest at much later stages and in already-established markets.

The venture capital industry, which has nurtured the growth of hundreds of high-technology companies such as Apple Computer, Genentech and Lotus Development, is shifting its focus to more mundane investments that have little to do with technological innovation or creating new jobs.

Discount stores, pizza shops, athletic apparel concerns and a host of companies that provide personal and business services are increasingly competing for funds with biotechnology ventures and computer concerns.

At the same time, more than a third of the $3.4 billion raised by venture capitalists last year [1986] appears to have been earmarked for leveraged buyouts, in which loans used to finance the acquisition of a company are secured with the assets of the company being acquired. Such buyouts invest in established companies rather than underwriting new ones.

”It may not be good for the country, but the fact is that technology has not been as rewarding as other forms of investment,” said Kenneth W. Rind, a partner in Oxford Partners, a large venture capital firm in Stamford, Conn. (New York Times, “High Tech’s Glamour Fades for Some Venture Capitalists”, 2/6/1987.)

America’s venture capital industry has been restructuring itself in a way that is eroding its historic role as a source of seed money…venture capitalists have been putting a greater share of their money in later-round financings and LBOs.29

From none in 1980, LBOs grew to 23% of VC dollars by 1986. Seed and early-stage financing, once a quarter of VC investment, fell to 12.5% by 1988.

| VC investment by type of financing | |||

|---|---|---|---|

| Seed & Start-up | Expansion & Late Stage | LBO | |

| 1980 | 25.0% | 75.0% | 0.0% |

| 1981 | 22.6% | 77.4% | 0.0% |

| 1982 | 20.0% | 68.0% | 12.0% |

| 1983 | 17.2% | 70.8% | 12.0% |

| 1984 | 21.0% | 67.0% | 12.0% |

| 1985 | 15.0% | 69.0% | 16.0% |

| 1986 | 19.0% | 58.0% | 23.0% |

| 1987 | 13.0% | 69.0% | 18.0% |

| 1988 | 12.5% | 67.5% | 20.0% |

Source: Gompers, “Rise and Fall”, op cit.

Many of the top firms moved either entirely or partly to LBOs: J.H. Whitney & Co. (one of the original VC firms, in the business since 1946); Patricof Associates (Alan Patricof returned to the VC fold in 2006 with his current fund Greycroft Partners); Welsh, Carson, Anderson & Stowe; Warburg Pincus; Merrill, Pickard, Anderson & Eyre; Bain Capital; and TA Associates were some of the more prominent. Even Sequoia started backing LBOs.

“We still want to invest in new ideas, but we will do it through more mature companies.”

— John Hesse, Plant Resources Venture Funds, Jan. 199030

VCs also funded rollups.

Instead of backing entrepreneurs to develop new companies, many deal makers are emphasizing investments in companies that plan to grow through acquisitions…the growth of the venture capital industry is making it harder to find worthy new companies to support. So they have to find other place to put their money. (Wall Street Journal, “Venture Capital Turns to Mergers For Faster Growth and Lower Risk”, 1/7/1986.)

As veteran venture capitalist Fred Adler put it: “Venture capital has more parts than it used to. We’re a lot more flexible about how we use our money.” (ibid.)

Even when VCs were investing in startups, the companies were unlike the ones that had generated the phenomenal 1980 VC returns. The new wisdom was to lower risk by investing in well-understood, slower growth markets. VCs also limited risk by shunning technology.

Some of the hottest venture deals these days are being done in a field that is mostly low-tech or even no-tech: specialty retailing…most of these smaller outfits are trying to carve their niche with the same basic strategy of lavishing tremendous amounts of personal attention on the customer. To use the emerging buzzword, they seek to be “full-service” retailers. (Wall Street Journal, “‘Full-Service’ Specialty Retailers Draw Venture Capital”, 5/1/1989.)

VCs backed companies like Staples (founded 1985) and Starbucks (founded 1985), despite their high capital requirements and lack of barriers to entry.

In the past 12 months, venture capitalists have invested a hefty $18.5 million in Staples, Inc…but in the same period—apparently lured by [Staples’] initial success—an estimated $10 million has been invested in at least five competing start-ups. (Wall Street Journal, “Retail Start-Up Decides to Start Out Big”, 5/14/1987.)

As in the high-tech sectors, initial success was followed by over-funding.

One of the hottest venture capital investment ideas—bankrolling office-supply discount chains—is starting to sour. In the past two years, investors poured nearly $200 million into at least 16 office-supply “supermarket” chains. But today, the flood of entrants threatens a market-share war, and the result may be hard times. Several companies seem to be faltering, and at least two have closed. (Wall Street Journal, “Growth in Office-Supply ‘Supermarkets’ Threatens Tough War for Market Share”, 12/1/1988.)

Top funds, like US Venture Partners and NEA, moved “from their traditional high-tech portfolios into specialty retailing and consumer product investments.”31 VCs had always backed retail companies (Jiffy Lube in 1979, for instance) but the volume of these deals increased. Consumer was the largest single VC investment category, by dollars, in 1984.32 And it was the largest category of VC-backed IPOs in 1984, 1985, and 1986.33 One unnamed venture capitalist said in the Journal “Although the prospects for unusually big hits like Apple and Sun are small, you can get good results with greater consistency.”34 This turned out to be wishful thinking.

While consumer related and ‘other products and services’ grew as a percent of VC disbursements, semiconductors, computer hardware, and communication shrank. Software and services did not start to take off until the ’90s.

By the end of the decade venture capitalists started to admit that the attempt to create predictable returns had failed.

In the mid-1980s, many [venture capitalists] experimented with investments in such low-tech industries as specialty retailing. Results were generally disappointing, in part because the financiers often didn’t understand what they were getting into. (Wall Street Journal, “Venture Capitalists Find Low-Tech Firms Appealing”, 6/20/1991.)

VCs acknowledged their inability to get venture capital returns in low-tech businesses by investing in more low-tech businesses:

Seeking greater safety, some venture capitalists say they increasingly invest in food retailing and distribution, waste management and other areas where emerging technology generally isn’t a factor. (ibid.)

VCs disliked high-technology because the high-tech sectors of the day were poor candidates for venture. Investments in cable-TV and cell-phone infrastructure could never have achieved the types of returns that an Apple Computer or Genentech did, because they required so much capital. (Even though capital-intensive companies like Federal Express had gone on to be successful IPOs in the 1970s, they were still bad investments for their early backers.35 ) Early stage investors, what few remained by the late 1980s, lowered their sights to avoid being crushed by future capital requirements. In biotech they gave up even trying to build self-sustaining companies that might one day go public.

Instead of building corporations and taking them public one day, these venture capitalists now develop companies purely for sale to big corporations. They make smaller investments for shorter periods than in the past. More than ever…they limit their risks and focus on developing products rather than companies. (Wall Street Journal, “Biotech Start-Ups are Increasingly Bred Just to be Sold”, 7/19/1989.)

The VC investing landscape had, essentially, bifurcated. One group of VCs made small, earlier investments and tried to manage their risk by investing in established markets or by building products, not companies; another group made much larger, later investments and tried to manage their risk by investing in companies that were not “startups” at all.

The initial successes of the venture industry in the first half of the decade have led to an excess of “megafunds”—venture pools with hundreds of millions of dollars to invest. The sheer size of these funds has, in many instances, transformed seed capital from a primary activity to a marginal one. (Wall Street Journal, “Venture Capital’s New Look”, 5/20/1988.)

Venture capitalists’ job is to invest in risky projects. But after shying away from risk for years, VCs finally found there was no longer anybody willing to found a risk-taking company. The number of high-tech starts plummeted.

It looked, for a time, like high-tech was done. Marc Andreessen recently described the Silicon Valley he moved to in 1994:

It was dead. Dead in the water. There had been this PC boom in the ’80s, and it was gigantic—that was Apple and Intel and Microsoft up in Seattle. And then the American economic recession hit—in ’88, ’89—and that was on the heels of the rapid ten-year rise of Japan. Silicon Valley had had this sort of brief shining moment, but Japan was going to take over everything. And that’s when the American economy went straight into a ditch. You’d pick up the newspaper, and it was just endless misery and woe. Technology in the U.S. is dead; economic growth in the U.S. is dead. (New York Magazine, “In Conversation: Marc Andreessen“, 10/19/2014.)

But, as every good contrarian knows, things are darkest before the dawn.

Reboot, 1993-

I woke up early, couldn’t go back to sleep

Cause I had been thinking of where it all would lead…

There’s a big day coming, about a mile away

There’s a big day coming, and I can hardly wait.

– Yo La Tengo, 1993.

It changed fast. A headline in the Wall Street Journal in August 1991 moaned “Venture Capital Funding for Small Companies Plunges.”37 A year later the headline read “Venture Funds Regain Appetite for Start-Ups.”38 Start-ups were back in favor.

What happened? Well, you know what happened. The Internet happened.

In 1993, investor interest in…young companies often focused on the new media and communications industry segments. The spotlight on new media and the emerging information superhighway helped early stage companies. (Wall Street Journal, “Firms Backed by Venture Capitalists Do Well in IPOs”, 1/14/1994.)

The technologies enabling “New Media” were not new. AOL and Cisco were both formed in the ’80s. The fiber optics that became the backbone of the “information superhighway” had also been laid in the ’80s39 and the multimedia capabilities of PCs were the result of years of work.40

The catalyst for the 1990s revolution was the invention of the World Wide Web by Tim Berners-Lee in 1990. In January 1993, Marc Andreessen and Eric Bina released the first version of Mosaic, an open-source Web browser. Also in 1993, CERN announced the Web was free for anyone to use, at just the time when the NSF freed the academic Internet to connect with commercial networks. The 1990s had begun, high-tech was saved.

Consumer adoption of the Web created some early winners. AOL went public in 1992; Netcom in 1994; UUNet, Spyglass and Netscape in 1995; Lycos, Excite, Yahoo!, CompuServe, Infoseek, C/NET, and E*Trade in 1996; and Amazon, ONSALE, Go2Net, N2K, NextLink, and SportsLine in 1997. Then IPOs got crazy. Ten Internet IPOs in 1995 turned into 18 in 1996, 15 in 1997, and 40 in 1998; but in 1999 there were 272. Even in 2000 there were 148, despite the stock market crash of March of that year (in 2001 reality sank in and there were only 6 Internet IPOs.)41

The large early stock price gains by Netscape, Amazon, and others rewoke investors to the potential of technology stocks and they bid up any company that had any involvement with the Internet. Private tech companies took advantage of the market opportunity by going public and investors bought these up too. These companies could not yet be evaluated on objective measures like earnings, so investors used the rising stock prices as the rationale to keep buying. Anyone who questioned the sustainability of prices was told they just didn’t “get it.”42

Entrepreneurs and venture investors struggled to satisfy the appetite of IPO investors. They took startups to market before they had proved their long-term viability, and funded any startup that might be able to make it to the public markets quickly. Companies were funded with questionable markets, management teams, business models, and products.

Regardless, venture investors often made good money on these short-term bets. Venture returns hit heights they had never seen, not even in the high-flying ’70s.

Money poured into venture at a rate that belied the 1980s warnings that the industry would need to shrink to prosper.

And many more new funds were started to take the money.

In March 2000, some investors realized that some of the public Internet companies could not, under any reasonable growth and valuation assumptions, be worth what the market valued them at. They sold, and prices went down. Other investors, seeing prices go down, decided to cut their risk by also selling. Prices went down further. There was a brief rally and then investors lost their nerve. On March 27, 2000 the NASDAQ, where many of the Internet companies had listed their stock, closed at 4,959. By April 14, less than three weeks later, it had dropped more than 30%, to 3,321. The NASDAQ lost half its value by the end of the year. It has never, even after almost 15 years, returned to the highs of March 2000.

1980s, 1990s

The ’90s were a bubble. Investors bought stocks because they could sell into a rising market. VCs backed companies because they could take them public. Everyone took brash product and market risks because the public markets did not care about these sorts of risks. But the ’80s were not a bubble. Not every cycle is a bubble.

If the fatal flaw of the ’90s was hubris–“This time it’s different”–the fatal flaw of the ’80s was fear. Venture capitalists were afraid to take risks. Instead they invested in known markets, less ambitious entrepreneurs, and later-stage companies. But you can’t get great returns without taking big risks: risk and reward are correlated. In the ’90s entrepreneurs and investors took huge risks and got big returns. In the ’80s they tried to avoid risk and got nothing.

Today

A couple of weeks ago the New York Times said:

The economics of starting companies, and investing in them, has changed over the last 15 years, said Andy Rachleff, a founder of Benchmark Capital…Before the ascendancy of the Internet, he said, venture capitalists invested in areas that had high technical risk and low market risk. It took a lot of capital to get these companies off the ground, but the odds that the company would succeed were relatively high if the company could deliver on its technology promise. “Today,” he said, “it’s the opposite.”

For that reason, many of the larger, more established venture funds are investing later, writing larger checks after concepts have proved themselves. These firms, which include Andreessen Horowitz, Benchmark and Sequoia Capital, still account for the majority of all venture capital dollars. (New York Times, Venture Capital Is Looking for Ways to Outrun the Herd, 12/10/2014.)

Risk is uncertainty about the future. High technical risk means not knowing if a technology will work. High market risk means not knowing if there will be a market for your product. These are the primary risks that the VC industry as a whole contemplates. (There are other risks extrinsic to individual companies, like regulatory risk, but these are less frequent.)

Each type of risk has a different effect on VC returns. Technical risk is horrible for returns, so VCs do not take technical risk. There are a handful of examples of high technical risk companies that had great returns—Genentech,43 for example—but they are few.44 Today, VCs wait until there is a working prototype before they fund, but successful VCs have always waited until the technical risk was mitigated. Apple Computer, for example, did not have technical risk: the technology worked before the company was funded.

Market risk, on the other hand, is directly correlated to VC returns. When Apple was funded no one had any way of knowing how many people would buy a personal computer; the ultimate size of the market was analytically unknowable. DEC, Intel, Google, etc. all went into markets that they helped create. High market risk is associated with the best VC investments of all time. In the late ’70s/early ’80s and again in the mid to late ’90s VCs were comfortable funding companies with mind-boggling market risk, and they got amazing returns in exchange. In the mid to late ’80s they were scared and funded companies with low market risk instead, and returns were horrible.

Today is like the 1980s. There are a plethora of me-too companies, companies with a new angle on a well-understood market, and companies founded with the hopes of being acquired before they need to bring on many customers. VCs are insisting on market validation before investing, and are putting money into sectors that have already seen big exits (a sign of a market that has already emerged.)

Saying VCs used to take high technical risk and now take high market risk is both an overly optimistic view of the past—the mythical golden age of heroic VCs championing the development of new technologies—and an overly optimistic view of the present—gutsy VCs funding radical innovations that create entirely new markets. Neither of these things is true. VCs have never funded technical risk and they are not now funding market risk.45 The VC community is purposely avoiding risk because we think we can make good returns without taking it. The lesson of the 1980s is that no matter how appealing this fantasy is, it’s still a fantasy.

Tomorrow

People in the VC industry talk about the ’60s, when institutional venture capital took off. They talk about the ’70s, when iconic companies like Apple and Genentech were founded and the microcomputer industry emerged. They talk about the ’90s and the Internet bubble. They don’t talk about the ’80s; the ’80s are the missing piece of the puzzle. You can have lots of plausible theories about what venture capitalists as a class can do to get good returns, until you take the 1980s into account. Then you can only have one: the only thing VCs can control that will improve their outcomes is having enough guts to bet on markets that don’t yet exist. Everything else is noise.

The 1990s are not our map, the 1980s are. Don’t worry about irrational exuberance fueling a bubble, that is not what is happening. Worry about fear of risk. We know where that leads: once again straight into the ditch.

– Thanks to Justin Singer for reading drafts of this and helping me think it through.

Unattributed quote, Wall Street Journal, “Venture Capitalists Rush in to Back Emerging High-Technology Firms”, 3/18/1981. ↩

“Venture Capital Industry Resources,” Venture Capital Journal (July 1984), pp. 4-6. Cited in Bygrave & Timmons, p. 165 ↩

Gompers, Paul A. “The Rise and Fall of Venture Capital.” Business and Economic History 23.2 (1994) : 1–26. This paper is an excellent summary of venture capital pre-1990s, written just as the era was closing. ↩

Wall Street Journal, “Venture Capitalists Rush in to Back Emerging High-Technology Firms”, 3/18/1981. ↩

Wall Street Journal, “To Increase Profits, Venture-Capital Firms are Investing Earlier in Fledgling Concerns”, 10/31/1983. ↩

Wall Street Journal, “Venture Capitalists Rush in to Back Emerging High-Technology Firms”, 3/18/1981. ↩

Wall Street Journal, “Venture Firms Lack People of Experience”, 12/8/1983. ↩

Bygrave, William and Jeffrey Timmons, Venture Capital at the Crossroads

, 1992, p. 149. Although out of print, this book remains one of the best books on venture capital. You can buy it used on Amazon for as little as $4. ↩

During the 1980s. It’s interesting to note that for post-1990s-vintage venture funds there is a bias towards experience: follow-on funds vastly outperformed first-time funds in the period 1990-1999. Thompson Reuters, 2008 Investment Benchmarks Report: Venture Capital, figure 3.011. ↩

Wall Street Journal, “Recent Venture Funds Perform Poorly as Unrealistic Expectations Wear Off”, 11/8/1988. ↩

Gompers, Paul A., “Grandstanding in the Venture Capital Industry”, Journal of Financial Economics 42 (1996) 133-156. ↩

Wall Street Journal, “Venture Capitalists are Assuming Growing Roles in Firms They Fund”, 12/27/1984. ↩

The idea of a “dominant design” that signals product innovation giving way to process innovation comes from Utterback, James M., and William J. Abernathy, “A Dynamic Model of Product and Process Innovation”, Omega 3(6) (1975) 639-656. It is very well described for a business audience in Mastering the Dynamics of Innovation

, an invaluable book. ↩

Wall Street Journal, “As Software Products and Firms Proliferate, a Shakeout is Forecast”, 2/23/1984. ↩

Wall Street Journal, “In Venture Capitalism, Few are as Successful as Benjamin Rosen”, 11/28/1984. ↩

Wall Street Journal, “New Computer Firms, Font of Big Fortunes, Grow Increasingly Rare”, 9/8/1989. ↩

Forbes, “Enzyme Eaten Jeans”, 10/29/1990; cited in Bygrave and Timmons. ↩

Wall Street Journal, “Parallel Processing Computers Attract Crowd of Investors Despite Limited Uses,” 10/5/1990 ↩

Winchester disk drive industry stats from Sahlman, William A., and Howard H. Stevenson. “Capital market myopia.” Journal of Business Venturing 1985 : 7-30. ↩

Wall Street Journal, “Recent Venture Funds Perform Poorly as Unrealistic Expectations Wear Off”, 11/8/1988. ↩

Burton J. McMurtry, quoted in O’Neill, Gerard K., The Technology Edge, p.238. ↩

Wall Street Journal, “Computer Industry Called Ripe for Mergers”, 6/19/1985. ↩

Disk drive company Connor Peripheral, for example, was founded in 1985 and went public in 1988. It produced an excellent return for its VCs. ↩

New York Times, “High Tech’s Glamour Fades for Some Venture Capitalists”, 2/6/1987. ↩

Cisco went public in 1990 and was one of the best performing IPOs of the ’90s. But what was a $6.4 billion revenue company by 1997 was in 1990 only $69 million in revenue. It raised venture only once, in 1988, from Sequoia. The company’s prospects were so iffy at the time that the founders had to sell a controlling interest to Sequoia, who turned around and ousted them before the IPO. ↩

Wall Street Journal, “Recent Venture Funds Perform Poorly as Unrealistic Expectations Wear Off”, 11/8/1988. ↩

Bygrave & Timmons, p. 29 ↩

Wall Street Journal, “Venture Capital’s New Look”, 5/20/1988. ↩

Wall Street Journal, “Venture Capital’s New Look”, 5/20/1988. ↩

Wall Street Journal, “Venture Capital Dims for Startups, but Not to Worry”, 1/24/1990. ↩

Wall Street Journal, “Consumer-Product Funds Give Giants Early Look at New Items”, 8/15/1985. ↩

National Science Foundation, Science & Engineering Indicators – 2002, Appendix Table 06-19. ↩

Venture Capital Journal, “Special Report: 96 Venture Backed IPOs in 1986–The Most Active Year Since 1983”, February 1987. ↩

Wall Street Journal, “Full-Service’ Specialty Retailers Draw Venture Capital”, 5/1/1989. ↩

The first $25 million in venture funding for Federal Express was crammed down in a pay-to-play funding in 1974. Venture Capital Journal, “More Money for Federal Express”, April 1974, p. 2. ↩

Wall Street Journal, “Venture Capitalists Find Low-Tech Firms Appealing”, 6/20/1991. ↩

Wall Street Journal, “Venture Capital Funding for Small Companies Plunges”, 8/1/1991. ↩

Wall Street Journal, “Venture Funds Regain Appetite for Start-Ups”, 9/21/1992. ↩

The Wall Street Journal, in September 1986, said: “If industry plans succeed, fiber optic technology soon will vastly increase the capacity of of the U.S. long-distance telephone system…this fiber optic system will blaze telecommunication’s path into the 21st century.” Wall Street Journal, “Fiber Optics Promises High-Tech Revolution,” 9/9/1986. ↩

Wall Street Journal, “Vast Changes Loom As Computers Digest Words, Sounds, Images,” 6/7/89. ↩

IPO data compiled by Prof. Jay Ritter, Univ. of Florida. ↩

I can’t do justice to this late 1990s mindset here, that is another post. It was somewhat ludicrous even at the time and even to those of us who were true believers in the enormous importance of the Internet. ↩

The history of Genentech shows pretty clearly that VCs are explicitly uncomfortable with technical risk. A great read on this is Sally Smith Hughes’ Genentech: The Beginnings of Biotech. ↩

Why this should be so is a pretty interesting question in itself. I’ve floated several hypotheses to friends but have nothing compelling. ↩

This is a macro view. Of course VCs have funded companies that have high technical risk, and of course VCs fund companies that have high market risk. But it is not what they are doing generally. ↩

Fascinating and fantastic. Thanks to both you and Justin for taking the time to do such a quality piece.

I’m keen to read more. Are there any particular books / papers you’d recommend, either from those within your footnote or beyond?

Great research. Vert interesting.

This is so damn good. Thank you.

Excellent piece, Jerry. Thanks.

This is brilliant! Insane amount of research, one of the most comprehensive articles on VC’s that I have read, and most importantly full of insights and relevant takeaways

Interesting review of lots of history. If I had a couple of additions, I’d single out Gary Morgenthaler, who in the 1970’s almost single-handedly convinced Congress to reduce the capital gains tax, and really helped this industry at a key time. And I’d look at the one constant over the years, which is that more than 100% of the gains are posted by a very small number of firms or even investors. For decades, it’s been a very asymmetric business.

Unbelievable good read. Couldn’t put it down. Thank you for the time and effort you (all) put into this.

Thanks for pulling this together. Some of the analysis is particularly helpful in current circumstance.

I will quibble, challenge, the early history suggestion that Volcker’s actions “worked.” This link to an article my father wrote as the Fed transitioned to Greenspan says it better than I might: https://gpbrockway.wordpress.com/2012/12/11/vale-volcker/. It examines Volcker’s Fed contributions in terms of five factors, (1) inflation, (2) general welfare, (3) economic output, (4) foreign trade, and (5) the deficit and then looks more closely at his underlying theory.

Thanks for all the research. This has to be the single best “connect the dots” piece on the web!

Outstanding read. Just wanted to say thank you for a wonderful article.

Thank you for this. As someone who entered the VC funded high-tech business in the early ’70s and lived through much of this either as an entrepreneur or investor I think you’ve captured the most important features of the business and its cycles.

At the root of what has happened is a fundamental transformation of a series of gigantic consumer markets by technology. While some of these transformations took place in the supporting infrastructure, the brilliance of some in the companies and investment groups is that they recognized that the infrastructure market would remain a small fraction of the size of the consumer markets it supports.

What many have underestimated is the magnitude of the gains to be made through these consumer market transformations and how radically and continuously they can be changed. It will be very interesting to watch as this current pool of money is invested.

In the 1998-2000 boom, VCs poured dollars into marketing in order to own a brand on the Internet, a brand for toys, for fragrance, for cars, for jewelry, for anything. The investments were often on top of non-existent business models. It was more important to own the brand in the new frontier because, with enough consumers, the business would work itself out. Then the bust.

In today’s froth, scale has replaced brand as the reason to pour dollars into a startup. In spite of the enormous amount of available VC capital, there is not nearly as much need for capital now. All the infrastructure is in the cloud and the R&D timeframe is days and weeks to prototype, not months and years. Startups can test and refine business models for much less than $1m.

To rationalize $1b rounds, VCs assume that companies like Uber have crazy market opportunities and need to scale yesterday. This is similar to the turn of the millennium when VCs assumed owning the online brand was salient investment goal. The difference is that today’s businesses have viable models so that, when a market correction comes, when the market realizes all these companies won’t scale to meet the investor’s fantastic needs, at least the companies will stay in business. VCs investors will have low returns, but the public markets are less likely to crash.

As a veteran of the 1970’, 1980’s and beyond, I can point to three major transitions in the 1980’s that affected almost every technology venture:

1.The emergence of the long-term effects of Moore’s Law that resulted in the development of the PC, which broke the IBM monopoly and democratized computing in ways we couldn’t imagine previously.

2.The maturing of the TCP/IP protocol (winning over the 7-layer bureaucracy) and the ability to easily connect to the Internet, which broke the lock-in protocol strategy of the 1970’s and was the foundation for the Internet explosion of the 1990’s.

3.The maturing of the relational database model, which dramatically speeded up software development and enabled the emergence of “big data” applications.

Great analysis Jerry, nicely done amigo.

And for the ´20s (in the 21st century!) the defining trend is how VC´s are taking VC-ing global. The likes of Sequoia are turning in their multiple-X´s far away from the Valley, the hedge funds types (Tiger Global) are placing even bigger bets in virgin territories (think India) and most interesting of all, local entrepreneurs are turning into VC´s (think Alibaba Group, Bharti Group) after doing their own IPO´s first.

Thank you for this fabulous reading!

Thanks for the writing and sharing mind. The logic stand point of technology risk and market risk is backed with induction and facts. Love this article.

Thanks you again

Great, great post. If I had one minor disagreement it would be about the 79s being a desert. I think it was when giants such as KP and Sequoia validated the VC business. You could have done a similar story in the 70s and even 60s. For those interested, you could see my perspective about the VC history on a slideshare document: A history of venture capital